With Y Combinator Demo Day upon us, ’tis the season of $2 million on $20 million cap SAFEs. While many investors have been vocal against such raises, YC partners generally stand by them and even YC founder Paul Graham is vocal with his defense.

As a longtime seed investor, I’ve seen many founders make fundraising decisions without realizing the long-term impacts on their companies. With a number of seed investor models out there, it’s important for founders to understand the underlying incentives and biases of different investor archetypes, ranging from YC to seed firms to multistage firms.

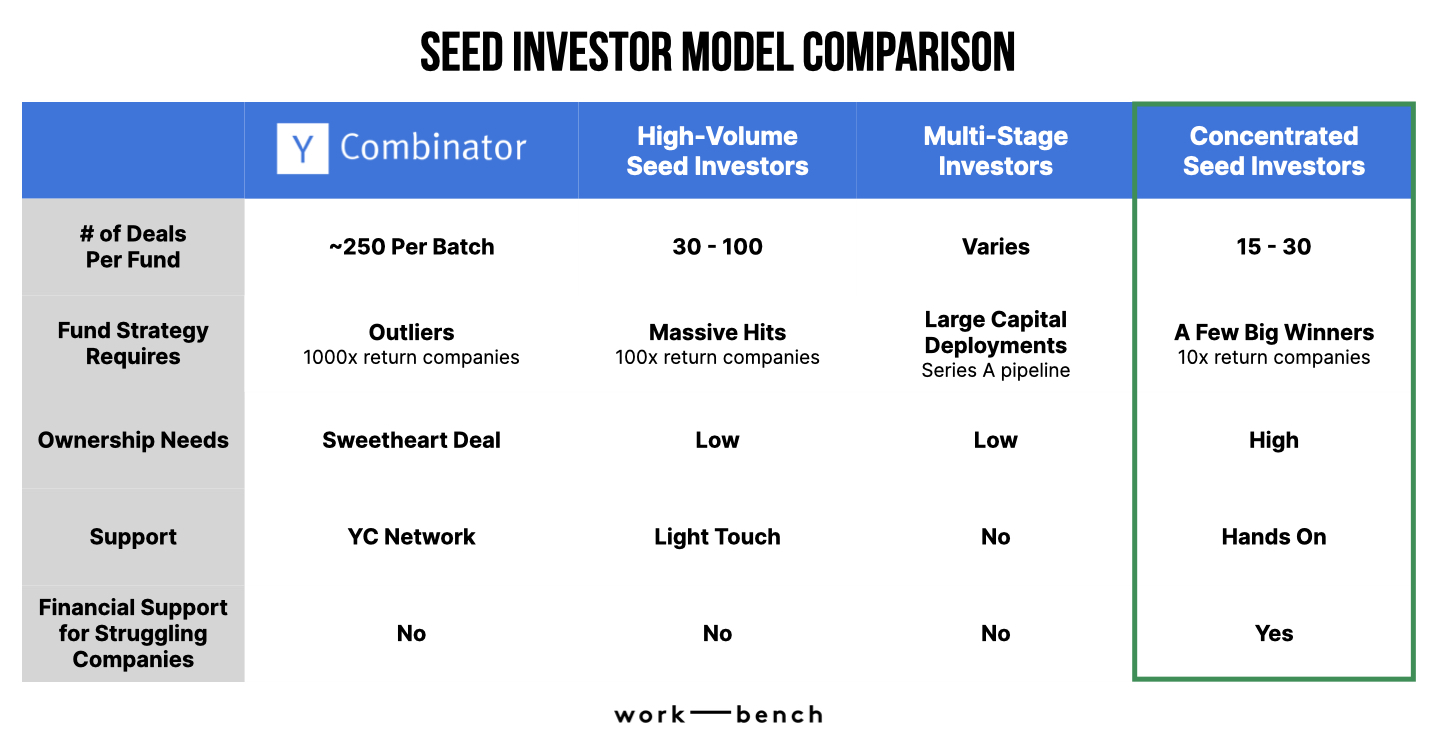

To summarize my takeaways, I created the following table, which I walk through in greater detail below:

Seed investor model comparison. Image Credits: Work-Bench

Y Combinator

There’s no debating that in aggregate, YC is a strong credential for founders in their earliest days, and they have a great crop of winners. The question for early-stage founders becomes, “What’s the hidden cost of fundraising from YC, and is the benefit evenly distributed?”

Companies that secure a spot in a YC batch not only receive a stamp of approval, but also gain access to a high-quality network of peers and alumni to learn from. In exchange, YC gets a sweetheart deal, investing $125,000 for 7% of the company and then an MFN (Most Favored Nation) letting them invest $375,000 in the future at favorable terms.

What’s important to understand is that YC’s goal is around finding and investing in extreme outliers.

YC’s own Garry Tan recently shared that “we only make money when the company becomes huge and is actually valuable. Like Coinbase or Airbnb or DoorDash.” On the flip side, what happens to companies that aren’t rocket ships, especially in a post-ZIRP (zero interest rate policy) environment?

The answer is that they’re out of luck: The YC model is “survival of the fittest,” and struggling companies are likely to go extinct. While this strategy has proven successful for their financial model, it certainly influences how they advise and support companies.

Pricing too high at an early stage is rife with issues that can plague the company’s growth if it doesn’t operate to perfection.

Raising a $2 million SAFE at a $20 million cap, whether because of a YC partner’s advice or peer-induced fear of missing out (FOMO) from batchmates, limits the type of investor you can pitch (whether the company realizes it or not) and raises the bar for the milestones needed to raise a Series A.

Given that most Series A investors would look to at least 2x the valuation of the seed raise, consider the milestones that would be sought out in a scenario to justify a $20 million valuation doubling to $40 million, compared to a $12 million doubling to $24 million.

More so, when raising a $2 million on $20 million round, startups’ cap tables typically become populated with angel investors and two to three high-volume seed funds along with YC, and if they hit any snags in their journey, there’s no additional financial support for them.